Depressing news this weekend as the candidate representing the Clinton/Obama wing of the Democratic Party won the Democratic National Committee's chairmanship, defeating the candidate from the Sanders wing of the Party. I'm sure Tom Perez is a good guy, but the technocratic wing of the Democratic Party just got its ass handed to it in an election that was supposed to be Hillary Clinton's to lose. This does not augur well for the left's chances in 2018 or 2020. It would be nice to have an honest debate in this country between the hard right wing, represented capably by the GOP, and something approximating Western European socialism, but it appears that is not to be. Of course, we will see how the DNC unfolds under Perez. Perhaps he will surprise us all.

Elsewhere: Barbara Ehrenreich, author of "Nickel and Dimed," has a nice short piece on the old, defeated working class of lore, many of whom voted for Donald Trump, and the future of the working class generally. Ehrenreich makes some very basic points that nonetheless are frequently lost and worth repeating:

- One, the working class is no longer strictly white (in fact, it never was, but it's even less so today).

- Secondly, the jobs of today are non-unionized, low-wage and not in manufacturing, by and large.

- Thirdly, job retraining is a bunch of bunkum. It's been tried and works very poorly, despite how swell it sounds. Sometimes you can't teach an old horse new tricks. Given that, do you simply let the horse die, or try to provide for it in some way?

- Fourthly, the energy of labor is largely based around unofficial campaigns such as that for an increase in the national minimum wage, whereas the AFL-CIO frequently plays a role in suppressing upstart labor movements which it sees as inconvenient or a threat in some way.

None of that should be news, but these points are often lost in how we talk about the working class, as though it were a strictly white, factory-based class, falling behind the arrogant class of doctors, lawyers, and other "professional" types who are wildly successful. It's a view of the world that contains glimmers of reality, but in its narrow focus distorts reality, and it's one we should retire.

This article on the modern labor force is worth reading, though of course, I will attempt to highlight the best bits for you young urban professionals on the go. Emphases added mine.

First of all, we're all nurses now:

But the forecasters were wrong in the most important respect. Workers

continue to find work, but now the jobs are in service. Taking care of

aging baby boomers, in particular, has become by far the largest driver

of job growth in the American economy. Among the occupations the Bureau

of Labor Statistics expects to grow most rapidly over the next decade:

physical-therapy assistants, home health aides, occupational-therapy

assistants, nurse practitioners, physical therapists,

occupational-therapy aides, physician assistants. ... You get the idea.

Nine of the 12 fastest-growing fields are different ways of saying

“nurse.”

Because goods have become much cheaper over the decades, people are increasingly spending their disposable money on services (such as home nursing) rather than material objects. These jobs are difficult to automate - would you pay extra for a human nurse, rather than a robot nurse? Most of us would.

Secondly, these new jobs suck, and its mostly women doing them:

The Cassandras, however, were right to warn about poverty in the midst

of abundance. Personal-service providers — “servants,” as they once were

called — tend to be poorly paid. There is little job security; the

benefits are meager; the work is physically demanding and emotionally

draining. It is not particularly surprising that women and immigrants

have been more likely to take these jobs than native-born men. For many

of the caretaking service jobs, less than 10 percent of the work force

is male.

Oh, and, thirdly, they're likely to do these jobs their entire lives:

The wages of service work increasingly determine the welfare of the

American working class and, to a substantial degree, the broader

economy. But politicians have paid little attention. That’s partly

because Americans continue to view service work as a way station, not a

way of life. Teenagers get their first job at McDonald’s; mothers dip

back into the work force as receptionists; seniors make a little extra

money as Walmart greeters. The reality is that these are the kinds of

jobs millions of Americans hold for their entire working lives. And

increasingly, these are the jobs their children will perform, too.

Economic feudalism.

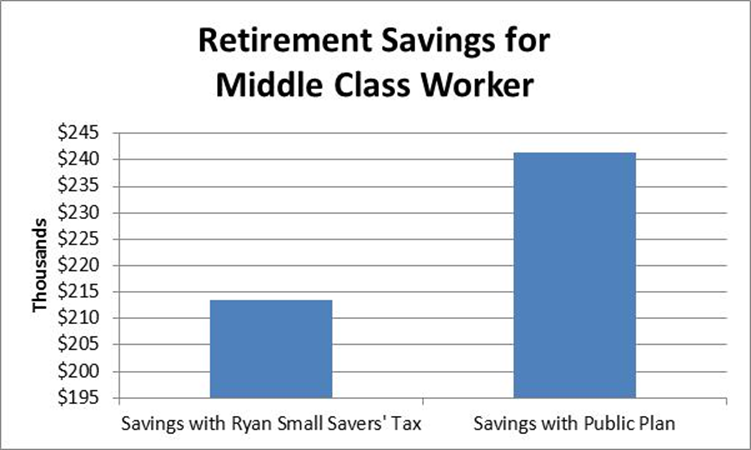

Moving away from labor for a minute: there is some interesting tax talk on the horizon.

I'll be giving this article a full run-down in a series of posts soon,

but for now I encourage you to read it. Some interesting ideas are

being kicked around. Some of them are terrible, but some are in fact

actually sound. In case of the TL;DRs, you don't need to start reading

the article until paragraph #6.

Finally, I want to present you Warren Buffett taking a big you-know-what on hedge funds.

Warren Buffett is often wrongly held up as a saint, or as a totally infallible investor, and he is neither of those things. But he is a stellar investor, and he does not mince words. It is telling that such a wildly successful investor does not speak in business jargon, designed to make the mortal man or woman feel like a clueless idiot, but instead, speaks in plain English.

He estimates that $100 billion in the last decade has been straight-up wasted by investors paying exorbitant fees to so-called experts. Just read this in its entirety, because it's gold, Jerry, gold:

“The

wealthy are accustomed to feeling that it is their lot in life to get

the best food, schooling, entertainment, housing, plastic surgery,

sports ticket, you name it,” Mr. Buffett wrote. “Their money, they feel,

should buy them something superior compared to what the masses

receive.”

“The

wealthy are accustomed to feeling that it is their lot in life to get

the best food, schooling, entertainment, housing, plastic surgery,

sports ticket, you name it,” Mr. Buffett wrote. “Their money, they feel,

should buy them something superior compared to what the masses

receive.”

He

continued, “The financial ‘elites’ — wealthy individuals, pension

funds, college endowments and the like — have great trouble meekly

signing up for a financial product or service that is available as well

to people investing only a few thousand dollars.”

Mr.

Buffett said that wealthy individuals get drawn in by consultants

selling them big promises. “Can you imagine an investment consultant

telling clients, year after year, to keep adding to an index fund

replicating the S. & P. 500?” he wrote. “That would be career

suicide. Large fees flow to these hyper-helpers, however, if they

recommend small managerial shifts every year or so.”

That

advice, Mr. Buffett added, “is often delivered in esoteric gibberish

that explains why fashionable investment ‘styles’ or current economic

trends make the shift appropriate.”

...

“Human behavior won’t change,” he wrote. “Wealthy individuals, pension

funds, endowments and the like will continue to feel they deserve

something ‘extra’ in investment advice. Those advisers who cleverly play

to this expectation will get very rich.”

Indeed. See you tomorrow!